All Categories

Featured

Table of Contents

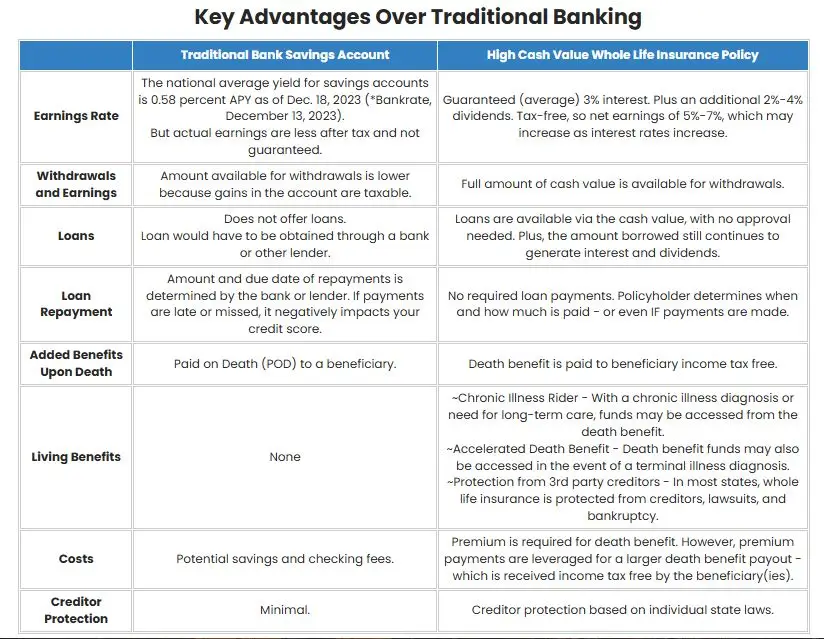

The are whole life insurance and universal life insurance. The money value is not added to the death benefit.

After one decade, the money worth has actually expanded to approximately $150,000. He gets a tax-free financing of $50,000 to begin an organization with his brother. The policy loan rates of interest is 6%. He pays back the funding over the following 5 years. Going this course, the rate of interest he pays returns right into his policy's money worth rather of a banks.

Visualize never ever having to worry about financial institution loans or high passion rates once more. That's the power of infinite banking life insurance.

There's no collection funding term, and you have the liberty to choose the repayment schedule, which can be as leisurely as settling the finance at the time of fatality. This adaptability reaches the maintenance of the finances, where you can go with interest-only payments, keeping the loan equilibrium level and workable.

Holding cash in an IUL fixed account being attributed interest can commonly be much better than holding the money on down payment at a bank.: You have actually always fantasized of opening your very own bakeshop. You can borrow from your IUL policy to cover the initial expenses of leasing an area, buying equipment, and working with staff.

Infinite Banking Illustration

Personal finances can be obtained from conventional banks and cooperative credit union. Below are some bottom lines to take into consideration. Bank card can supply a flexible way to borrow money for very short-term periods. Borrowing money on a credit report card is usually very costly with annual percentage prices of interest (APR) frequently getting to 20% to 30% or even more a year.

The tax therapy of plan fundings can differ considerably relying on your nation of residence and the particular terms of your IUL policy. In some regions, such as The United States and Canada, the United Arab Emirates, and Saudi Arabia, plan loans are typically tax-free, using a considerable advantage. Nonetheless, in various other territories, there may be tax obligation implications to take into consideration, such as possible tax obligations on the finance.

Term life insurance policy only supplies a fatality advantage, with no cash worth accumulation. This suggests there's no cash money worth to borrow versus. This post is authored by Carlton Crabbe, President of Resources for Life, a specialist in providing indexed universal life insurance policy accounts. The info supplied in this post is for instructional and informative functions only and need to not be understood as financial or financial investment guidance.

Whole Life Infinite Banking

When you first hear concerning the Infinite Financial Principle (IBC), your very first response might be: This appears as well great to be true. The trouble with the Infinite Banking Concept is not the concept yet those individuals using an unfavorable review of Infinite Banking as a principle.

So as IBC Authorized Practitioners through the Nelson Nash Institute, we believed we would certainly answer a few of the leading concerns individuals search for online when finding out and comprehending everything to do with the Infinite Financial Principle. So, what is Infinite Financial? Infinite Financial was created by Nelson Nash in 2000 and totally discussed with the publication of his publication Becoming Your Own Banker: Unlock the Infinite Financial Concept.

Chris Naugle Infinite Banking

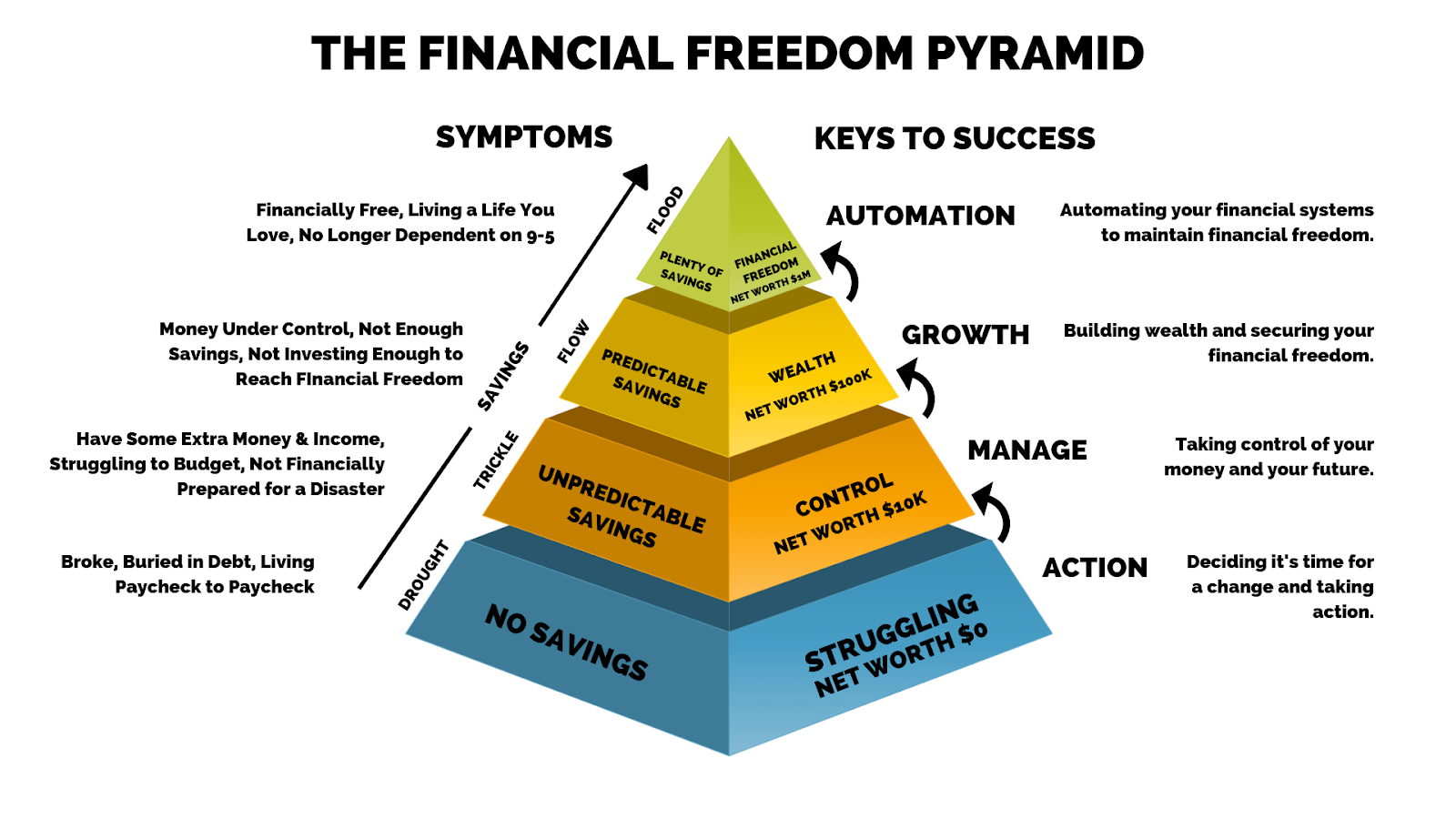

You think you are appearing monetarily ahead since you pay no passion, yet you are not. When you conserve money for something, it normally implies sacrificing something else and cutting down on your way of living in other areas. You can repeat this procedure, yet you are simply "diminishing your method to wide range." Are you satisfied living with such a reductionist or scarcity attitude? With saving and paying money, you might not pay passion, however you are using your money once; when you invest it, it's gone permanently, and you give up on the opportunity to gain lifetime substance rate of interest on that cash.

Even banks use entire life insurance coverage for the exact same functions. The Canada Earnings Firm (CRA) also identifies the worth of getting involved whole life insurance policy as an one-of-a-kind possession course utilized to produce lasting equity securely and predictably and give tax obligation benefits outside the range of typical investments.

Universal Bank Unlimited Check

It allows you to generate wealth by satisfying the banking function in your very own life and the capability to self-finance major way of living purchases and expenditures without interrupting the compound rate of interest. Among the most convenient methods to believe concerning an IBC-type getting involved entire life insurance plan is it is similar to paying a home mortgage on a home.

When you borrow from your getting involved entire life insurance coverage policy, the money value proceeds to expand undisturbed as if you never borrowed from it in the first location. This is due to the fact that you are making use of the cash value and death benefit as security for a loan from the life insurance firm or as collateral from a third-party loan provider (known as collateral financing).

That's why it's important to function with a Licensed Life Insurance coverage Broker accredited in Infinite Banking who frameworks your participating entire life insurance coverage plan correctly so you can stay clear of adverse tax obligation effects. Infinite Financial as an economic technique is not for everyone. Below are some of the pros and disadvantages of Infinite Financial you must seriously consider in deciding whether to progress.

Our recommended insurance provider, Equitable Life of Canada, a mutual life insurance policy firm, focuses on getting involved entire life insurance policy plans details to Infinite Financial. In a common life insurance firm, insurance policy holders are taken into consideration business co-owners and receive a share of the divisible surplus produced annually via returns. We have a range of service providers to pick from, such as Canada Life, Manulife and Sunlight Lifedepending on the requirements of our customers.

Please also download our 5 Leading Inquiries to Ask An Infinite Banking Agent Prior To You Employ Them. For additional information regarding Infinite Financial visit: Please note: The material given in this newsletter is for informational and/or academic objectives only. The details, viewpoints and/or sights expressed in this e-newsletter are those of the writers and not always those of the supplier.

How To Start Infinite Banking

The idea of Infinite Financial was produced by Nelson Nash in the 1980s. Nash was a financing specialist and fan of the Austrian institution of economics, which promotes that the worth of goods aren't clearly the result of typical financial structures like supply and demand. Rather, individuals value money and products differently based upon their financial condition and needs.

One of the mistakes of traditional banking, according to Nash, was high-interest prices on fundings. Way too many individuals, himself consisted of, entered into economic difficulty as a result of dependence on financial organizations. Long as banks established the passion prices and loan terms, people really did not have control over their own wealth. Becoming your own banker, Nash established, would put you in control over your monetary future.

Infinite Financial requires you to possess your economic future. For goal-oriented people, it can be the best financial device ever. Here are the benefits of Infinite Financial: Probably the single most beneficial facet of Infinite Banking is that it enhances your cash flow.

Dividend-paying whole life insurance coverage is extremely low risk and offers you, the insurance policy holder, a lot of control. The control that Infinite Financial uses can best be grouped into 2 classifications: tax obligation benefits and possession securities. Among the reasons whole life insurance policy is perfect for Infinite Financial is just how it's exhausted.

Whole life insurance policy policies are non-correlated properties. This is why they function so well as the financial foundation of Infinite Financial. Despite what happens in the marketplace (stock, property, or otherwise), your insurance coverage preserves its well worth. Way too many people are missing out on this essential volatility barrier that helps protect and grow wide range, rather dividing their money into two buckets: financial institution accounts and financial investments.

Market-based investments grow wealth much quicker however are exposed to market variations, making them inherently high-risk. Suppose there were a third pail that provided safety and security but also moderate, guaranteed returns? Whole life insurance coverage is that 3rd bucket. Not just is the price of return on your entire life insurance plan guaranteed, your survivor benefit and premiums are additionally ensured.

Royal Bank Infinite Avion Points

Infinite Banking appeals to those looking for higher economic control. Tax efficiency: The money worth grows tax-deferred, and plan fundings are tax-free, making it a tax-efficient device for constructing riches.

Property protection: In numerous states, the money value of life insurance policy is secured from creditors, adding an additional layer of economic safety and security. While Infinite Financial has its qualities, it isn't a one-size-fits-all solution, and it includes significant downsides. Below's why it may not be the most effective technique: Infinite Banking typically needs complex policy structuring, which can confuse policyholders.

{kind=link}

Latest Posts

Infinite Banking Concept Updated For 2025

Infinite Concept

Be Your Own Bank Life Insurance